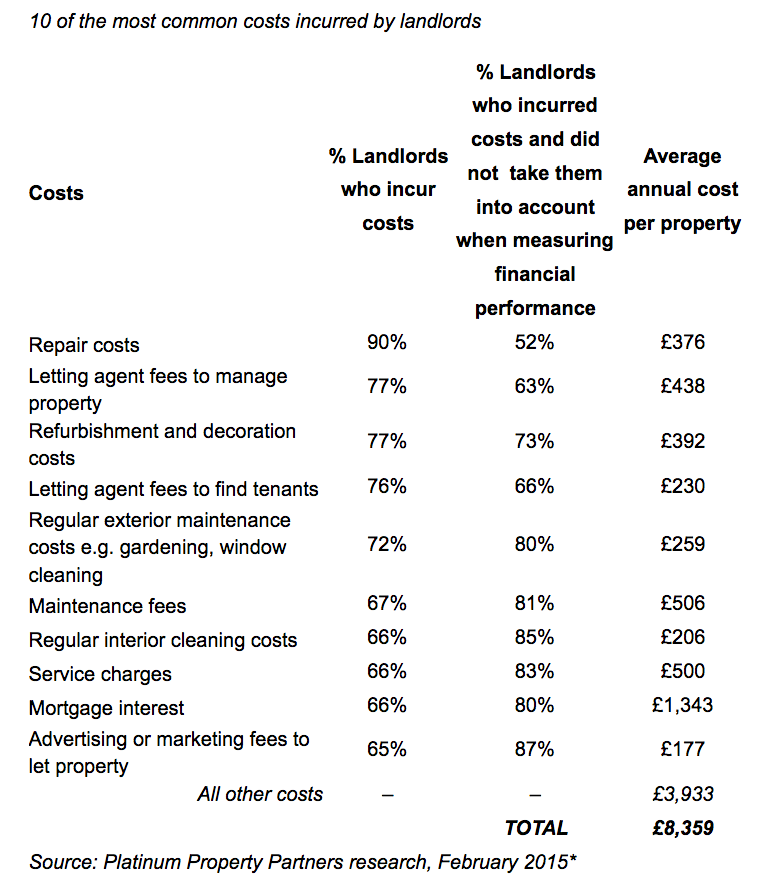

There have been numerous research papers written over the years looking at what landlords budget for when taking on a buy-to-let property, and the results are surprising. Of those who incurred costs, over 50% had made no provision for repairs, 73% disregarded potential decorating charges, and 80% ignored mortgage interest they’d be liable for!

This is clearly no way to run a business, so we thought we’d give you a quick checklist of common costs that many landlords forget to budget for. Our list will help you correctly calculate the true cost of your next buy-to-let investment and give you a solid idea on whether or not the property will be as profitable as you need it to be.

Shall we begin?

1. Insurance

The vast majority of lenders will want to see that your property has adequate cover in the form of buildings insurance before they agree to give you a mortgage. This is entirely understandable, and something you should want to have for your own peace of mind. Building insurance will cover you for any unforeseen events such as floods or fires, and enable you to claim back any financial losses you may incur due to structural damage caused by such catastrophes.

While it isn’t required by lenders, many landlords choose to take out contents insurance as well, which covers the fixtures and fittings found within a property. Some landlords mistakenly assume that as they are renting out their property unfurnished, contents insurance isn’t necessary, but this isn’t the case. Don’t be one of those who receive a nasty shock when you have to completely replace a kitchen or bathroom with your own hard-earned cash!

2. Letting agent’s fees

Depending on the level of management service you opt for, letting agent’s fees will vary considerably, but that doesn’t mean you should disregard the cost from your calculations altogether! Typically, a full management service will cost you somewhere in the region of 10% to 15% of the rent your tenant pays, so it’s an important expense to factor into your sums.

Many landlords will consider a property to be a viable investment if they are clearing their mortgage payments and making a little extra on top, so failing to take into account a 15% charge can be devastating. Not only that, opting for a property with such tight margins can lead to other problems, which leads us nicely to cost #3…

3. Void periods

Regardless of whether you have a tenant in situ or not, your lender is going to be holding their hand out each and every month, so failing to factor in void periods can be a fatal flaw in a lot of landlord’s calculations.

Other bills will keep on coming, too. Things such as utilities still need to be paid, so you should definitely be aware of the impact an empty property can have on your finances. To be on the safe side when running your annual numbers, multiply your monthly rental income by 11 instead of 12 to give your calculation a month’s void period buffer.

4. Repairs and replacements

As we touched upon in our intro, over half (52%) of landlords do not factor in the potential cost of repairs when they are calculating the viability of a new buy-to-let property. Landlords are responsible for the upkeep of all appliances they provide their tenants with, so this isn’t something to leave off of your list.

Repairing, or in some instances replacing, items such as white goods can make a hefty dent in your annual income. Factoring in a few hundred quid when making your annual calculations will help ease your repairs and replacements pain. In fact, many savvy landlords physically put away money each month to cover any problems that may arise.

5. Maintenance

Getting a handle on exactly how much maintenance will cost you isn’t easy, but it certainly shouldn’t be ignored. Things such as ground rent and service charges, if you are looking at a flat, will be set, but other costs will be variable. Things such as furnishings upkeep, decorating costs, pre-rental cleaning, etc. are harder to put a concrete figure on, but you must always add something for maintenance to your overall costs to help lessen the blow should they be required.

Another thing to remember when considering maintenance costs is your legal requirement to perform annual checks, such as gas safety. All appliances, gas fittings, and flues must be checked each year to ensure that they are in good working order, so be sure to add that to your figures as well.

Are you thinking of becoming a landlord in East London or West Essex? If you are, we can help! Give our friendly lettings team a call today on 020 8989 2091 to find out exactly what we can do for you.